Pricing in the residential battery segment was mixed in June, with the performance category pulling back sharply while premium systems moved higher.

- High-voltage premium brands: €280.8/kWh (+3% vs May)

- High-voltage performance brands: €150.5/kWh (–6% vs May)

- Low-voltage brands: €108.6/kWh (–1% vs May)

The high-voltage performance segment recorded its largest monthly decline of the year, extending the correction that began in May after April's sharp increase driven by Deye and Growatt pricing activity. Premium high-voltage systems, by contrast, edged back up in June, moving further away from April's cycle low. Low-voltage batteries saw only a marginal decline, continuing the gradual softening trend visible since March.

June PV Index: premium modules hit new highs, confidence holds firm

Top 5 battery brands: June 2026

Dyness climbs to the leading position in the residential battery ranking for June, up from third place in May. The brand's continued strength across modular residential platforms drove the move to the top of the ranking.

Deye holds second place, maintaining consistent momentum after topping the ranking in May. Sungrow returns to third on a strong rebound in transaction activity, while Huawei slips to fourth. Pylontech rounds out the Top 5.

Overall, June brought another significant reshuffle at the top of the residential ranking, with Dyness overtaking Deye after a strong month of marketplace activity.

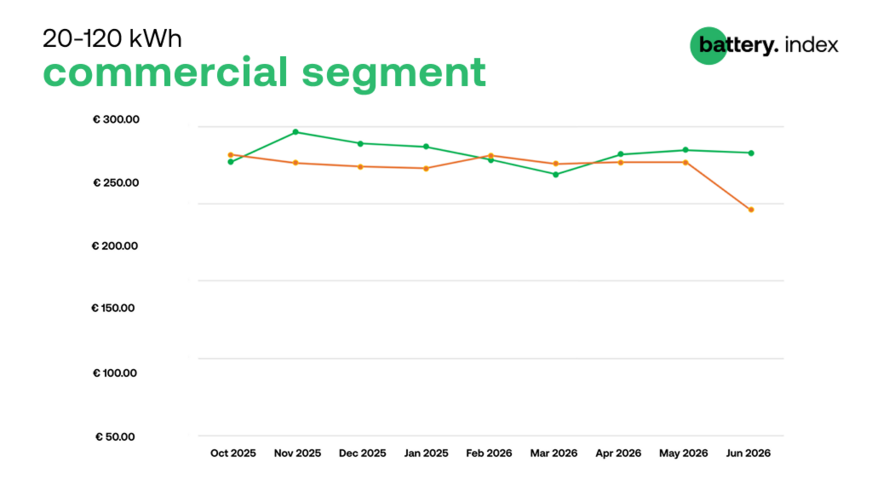

Commercial segment (20–120 kWh): offer volumes rebound in the smaller segment

Marketplace activity in the commercial and industrial storage segment picked up in June, particularly in the 20–30 kWh range, while average pricing in the 60–120 kWh category dropped sharply.

- 20–30 kWh systems: €232.4/kWh (–1% m/m)

- 60–120 kWh systems: €195.7/kWh (–14% m/m)

The number of active offers in the 20–30 kWh range rose to 84, up 8% month-on-month, reversing the gradual decline seen since February. Pricing in this segment remained broadly stable, easing only slightly compared with May.

sun.store

The 60–120 kWh segment told a different story: while the number of active offers also increased slightly, to 26, average pricing fell sharply. The decline was driven mainly by the disappearance from the marketplace of the product with the second-highest unit price in this category, rather than by a broader repricing of the segment.

Most offered products – June 2026

20–30 kWh segment

The smaller commercial segment remains dominated by modular high-voltage tower systems, with a strong presence of BYD's HVB configurations across multiple capacity tiers.

- Dyness Tower Pro TP23

- Sungrow SBH200

- Huawei LUNA2000-21-S1

- Fronius Reserva Pro 24.0

- BYD HVM+ 22.1

- BYD HVB 29.6

- BYD HVB 26.7

- BYD HVB 23.7

- BYD HVB 20.7

60–120 kWh segment

The larger commercial storage segment remains concentrated around a small number of integrated platforms, with Deye and Dyness continuing to dominate.

Deye GE-F60

Dyness BF100-C100

KSTAR KAC50DP-BC100DE

Growatt AXE 60.0H-1HC-E1

Dyness DH100F-C100

Deye BOS-G80 Pro

Deye BOS-G60 Pro

Deye GE-F60 remains the most represented product in the 60–120 kWh range for a fourth consecutive month, consolidating its position as the marketplace's leading commercial storage platform.

May Battery Index: residential decline, commercial standstill

Battery price trends Europe 2026 – the key takeaways

- High-voltage performance batteries recorded their steepest decline of the year, down 6% month-on-month

- Premium high-voltage systems moved higher, breaking a multi-month softening trend

- Dyness took the top spot in the residential brand ranking, with Sungrow climbing back to third place

- Commercial offer volumes in the 20–30 kWh segment rose 8%, reversing several months of contraction

- Average pricing in the 60–120 kWh segment fell 14%, driven by the exit of a high-priced product from active listings rather than a broader market correction. (hcn)