Prices in the residential battery segment rose across premium, performance and low-voltage systems:

- High-voltage premium brands: €284.9/kWh (+4% vs January)

- High-voltage performance brands: €155.4/kWh (+5% vs January)

- Low-voltage brands: €112.3/kWh (+9% vs January)

Premium high-voltage systems remain the most expensive option for residential installations, reflecting strong brand positioning and integrated system ecosystems. Performance-focused systems offer a significantly lower cost per kWh, while low-voltage batteries remain the most price-competitive option for installers pursuing cost-optimised residential projects.

February PV Index – TOPCon bifacial prices nearly 20 percent above 2025 low

Despite the February price increases, the structural gap between premium and value-oriented systems remains considerable, highlighting the pronounced segmentation of the European residential storage market.

Top 5 battery brands: February 2026

Sungrow leads the residential battery ranking, reflecting strong demand for its modular storage systems across European markets. Dyness takes second place, maintaining a solid presence in the mid-range segment. Deye ranks third, supported by growing adoption of its battery systems within hybrid inverter ecosystems. Huawei is in fourth place, while Pylontech completes the top five with its established modular battery platforms.

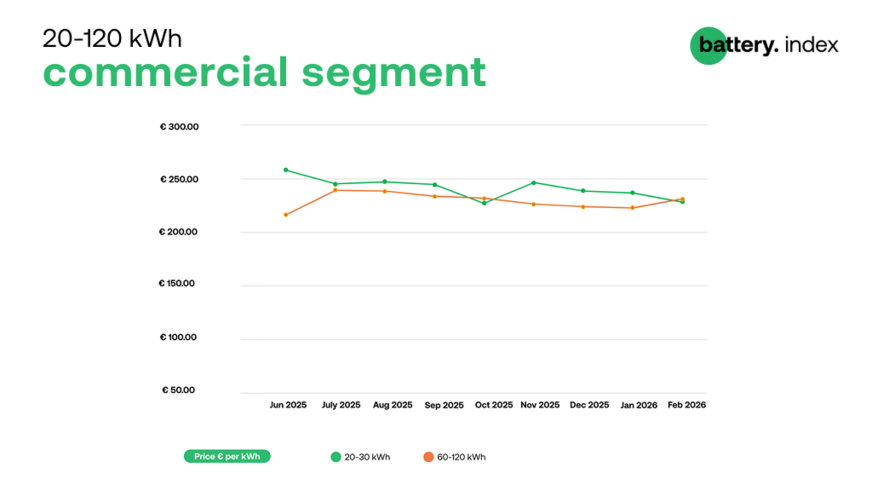

Commercial segment (20–120 kWh): stable pricing with moderate adjustments

Pricing in the commercial and industrial storage segment remained relatively stable in February.

- 20–30 kWh systems: €228.11/kWh (–4% m/m)

- 60–120 kWh systems: €230.83/kWh (+4% m/m)

Compared with the residential market, battery pricing in the C&I segment tends to change more gradually due to longer project development cycles and procurement planning. As a result, month-to-month price movements are typically moderate. At the same time, the number of active offers in the marketplace has continued to grow, signalling increasing product availability in the segment.

sun.store

Most offered products

20–30 kWh segment

- Dyness Tower Pro TP23

- Sungrow SBH200

- BYD Battery-Box Premium HVM 22.1

- Sungrow SBH250 PylonTech Force H3/409.6

- Dyness Tower T21 BYD HVB 29.6

The small commercial segment continues to be dominated by modular high-voltage tower systems, allowing installers to scale capacity depending on project requirements.

60–120 kWh segment

- Deye GE-F60

- Huawei LUNA2000-107-1S11

- Deye BOS-G60 Pro Solax

- AELIO-P60B100

- Solax AELIO-P50B100

This segment remains concentrated around a relatively small number of established platforms used in commercial and industrial storage projects. (hcn)