Pricing trends were more mixed at the segment level. TOPCon bifacial pulled back after May's sharp, size-driven jump, while TOPCon monofacial and the premium categories continued to climb. The inverter market saw only minor changes, with a gradual weakening in larger hybrid systems offset by price increases in the string inverter segment.

June brought a split market for module pricing. After TOPCon bifacial's sharp 7% jump in May the segment pulled back in June:

- TOPCon bifacial: €0.119/Wp (–5% m/m)

- TOPCon monofacial: €0.126/Wp (+4% m/m)

The pullback in bifacial pricing looks like a correction after May's outsized move, rather than a broader reversal in TOPCon demand. Monofacial pricing continued to edge higher over the same period.

Premium residential categories, meanwhile, kept pushing into new pricing territory:

- Full Black modules: €0.129/Wp (+1% m/m)

- Back Contact modules: €0.135/Wp (+1% m/m)

Back Contact modules extended their run as the most expensive segment in the index for a fourth straight month, though the pace of increase has clearly slowed compared with the sharp gains seen earlier in the year.

May PV Index – prices up, confidence up, inverters steady

Based on power sold, the Top 5 module brands in June were JA Solar, Trina Solar, LONGi, Jinko Solar and Canadian Solar. JA Solar overtook Trina Solar to reclaim first place after just one month at number two, while the rest of the ranking held steady. LONGi, Jinko Solar and Canadian Solar all retained their positions from May.

Inverters: price softening continues

Inverter prices moved only modestly in June, extending the broadly stable pattern seen since the spring.

Hybrid inverters

- 1–15 kW: €93.14/kW (–2% m/m)

- >15 kW: €78.53/kW (–1% m/m)

Both hybrid segments eased slightly in June, continuing the gradual downward drift that has been visible in larger systems for several months.

sun.store

String/on-grid inverters

- 1–15 kW: €43.23/kW (–2% m/m)

- >15 kW: €28.33/kW (+2% m/m)

Smaller string inverters softened slightly, while larger commercial systems ticked up again, extending the modest upward trend seen at the larger end of this segment since April.

Inverter brand rankings

Hybrid inverters

Deye and Huawei held their top two positions comfortably. Further down, Sungrow jumped back up to third place after dipping to fifth in May, while GoodWe and Fronius both slipped a rank.

String/on-grid inverters

Huawei and Sungrow again held the top two spots. SMA moved up to third place, swapping positions with Fronius, which slipped to fourth. SolarEdge remained in fifth for a sixth consecutive month.

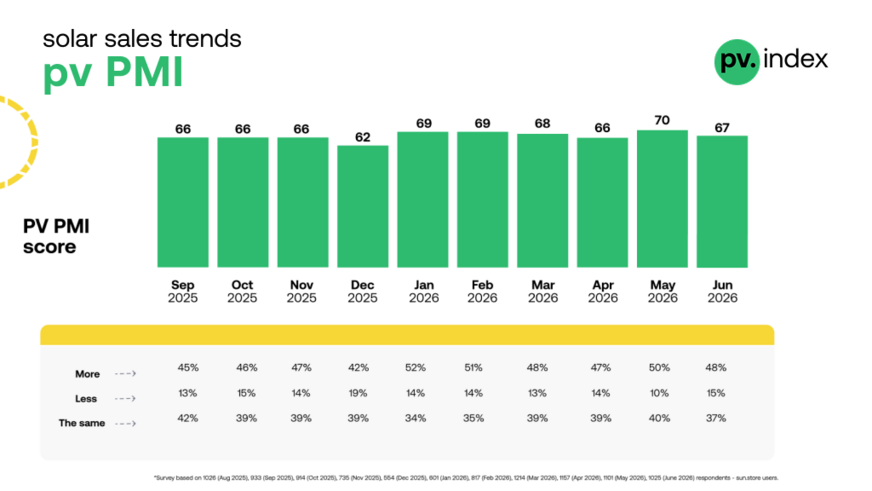

PMI: confidence stays firmly expansionary

The PV PMI came in at 67 in June, down from May's reading of 70, but still well above the neutral threshold that would signal a cooling market.

sun.store

Survey results from 1,025 sun.store users:

- 48% plan to buy more

- 37% expect no change

- 15% plan to buy less

The share of buyers planning to cut purchases rose back to 15%, up from May's low of 10%, though it remains well within the range seen over the past year.

After the spike – why solar and battery prices will cool again

What to expect

June's data points to a market that is consolidating rather than reversing course. A few things stand out from this month's data:

- Back Contact and Full Black modules extended their runs at the top of the index, confirming resilient demand for premium products

- TOPCon bifacial pricing corrected lower after May's sharp, size-driven spike, while monofacial kept climbing steadily

- JA Solar reclaimed the top spot in the module brand rankings after just one month behind Trina Solar

- Sungrow jumped back into third place in hybrid inverters, while SMA edged out Fronius for third in the string segment

- PMI eased to 67, still comfortably expansionary but off May's ten-month high

With buyers still willing to pay more for premium module categories and inverter prices remaining stable, the European photovoltaic market is entering the second half of the year on a solid footing. (hcn)