March saw a clear strengthening in module pricing, particularly in higher-efficiency and premium categories. The data indicate that demand remains strong enough to push prices higher across both TOPCon modules and premium, high-performance products.

TOPCon technologies continued their upward price trend:

- TOPCon bifacial: €0.107/W (+4% m/m)

- TOPCon monofacial: €0.114/W (+5% m/m)

This confirms that next-generation module technologies are continuing to strengthen their position in the European market. After several months of relative price resilience, TOPCon products are now trading well above mid-2025 levels, reflecting growing market acceptance and ongoing technological transition.

Stay informed – subscribe to our newsletters

Premium and design-oriented categories also saw further gains in March:

- Full Black modules: €0.114/W (+6% m/m)

- Back Contact modules: €0.118/W (+10% m/m)

The back-contact segment recorded the strongest growth among all monitored categories, underlining continued willingness to pay a premium for high-performance modules with strong design appeal. Full-black modules also posted notable gains, indicating that aesthetically oriented segments remain resilient in a price-sensitive market.

PERC modules remain unchanged at a benchmark of €0.077/W. As in previous months, limited trading depth in recent observations means the index should be interpreted with caution. The broader picture remains the same: PERC prices are no longer driving the market, as demand and pricing continue to shift towards newer technologies.

Expert comment: March increases may prove temporary

Krzysztof Rejek, VP of Sales at sun.store, says the price increases seen in February and March may not set the medium-term trend. In his view, distributor prices could remain around 20 percent above end-2025 levels in the short term, but there are growing signs that the recent rise may be temporary.

“In the short term, until the beginning of Q2, module prices at distributors may remain around 20 percent higher than at the end of 2025. However, more and more signals suggest that the February–March increase may be temporary.”

Stabilising market faces fresh uncertainty from geopolitical shifts

Rejek also notes that while March still brought further increases in TOPCon pricing, the pace of growth has already begun to slow.

“In Q2, price stabilisation or even a correction of several to more than ten percent is possible.”

According to Rejek, current price increases are driven mainly by manufacturers rebuilding margins and advance purchasing ahead of regulatory changes in China, rather than by structurally stronger demand. At the same time, weaker demand fundamentals and falling input costs could increase the likelihood of a correction later in the quarter.

“The removal of export tax relief in China (effective from 1 April) has a limited cost impact of around nine percent. Instead, current price movements are driven primarily by manufacturers rebuilding margins and by advance purchasing ahead of regulatory changes. At the same time, declining prices for cells, wafers and silver, combined with still relatively weak demand, increase the likelihood of a price correction in Q2.”

Brand rankings: clear reshuffle in module leadership

March saw another notable reshuffle among leading module brands, highlighting the continued dynamism of competitive positioning across European sales channels. Based on volumes sold, the top five module brands for March were:

- Trina Solar

- JA Solar

- Aiko

- LONGi

- TW Solar

Trina Solar moved into first place in March, supported by strong transaction volumes. JA Solar remained among the leading brands in second place, confirming that its February lead was not a one-off. Aiko recorded the biggest shift, rising to third and strengthening its market position. LONGi remained among the top players, while TW Solar entered the top five.

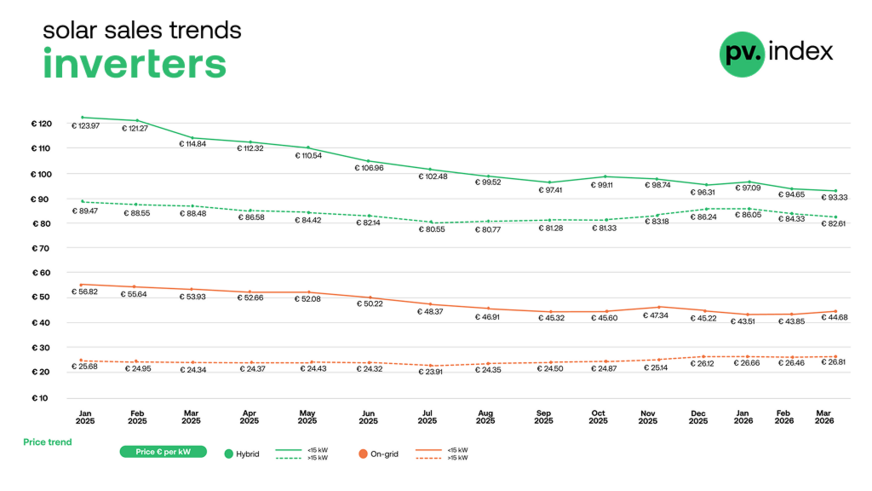

Inverters: small price moves, stable market structure

Inverter prices remained broadly stable in March, with little variation between segments. The main trend was clear: hybrid system prices edged down, while on-grid prices edged up.

Hybrid inverters

1–15 kW: €93.33/kW (–1% m/m)

15 kW: €82.61/kW (–2% m/m)

Hybrid prices continued to ease modestly in March. Demand for storage-compatible systems continues to provide structural support for this segment, even as competition has intensified.

sun.store

String / on-grid inverters

1–15 kW: €44.68/kW (+2% m/m)

15 kW: €26.81/kW (+1% m/m)

In the on-grid segment, prices rose slightly across both categories, suggesting the earlier correction phase has largely run its course, particularly in residential and commercial applications. Overall, grid-connected inverter prices remain stable, with no signs of significant downward pressure.

Inverter brand rankings: market leadership remains broadly unchanged

Hybrid inverters:

- Deye

- Huawei

- Fronius

- GoodWe

- Sungrow

Deye continues to lead the hybrid segment, supported by strong price-performance positioning and broad appeal for storage-ready installations. Huawei remains in second place, while Fronius, GoodWe and Sungrow continue to form the core of the leading group.

String inverters:

- Huawei

- Sungrow

- SMA

- Fronius

- SolarEdge

Huawei remains the leading brand in the string inverter segment, with Sungrow and SMA maintaining strong positions. Fronius and SolarEdge also remain firmly among the leading names in the category.

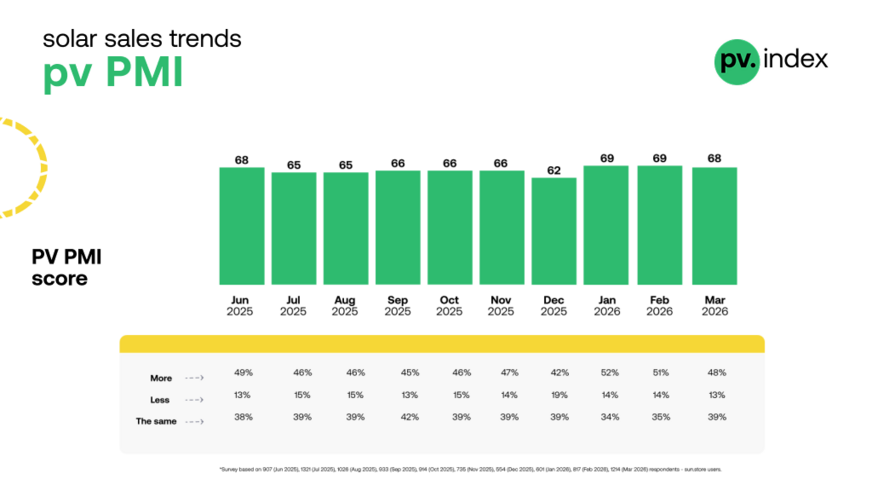

PV PMI: sentiment remains clearly positive

The PV Purchasing Managers’ Index reached 68 in March, confirming that market sentiment remained firmly in expansion territory even after the exceptionally strong February reading.

Survey results among 1,214 sun.store users show:

- 49 percent expect to increase purchases

- 39 percent expect no change

- 13 percent expect reduced purchasing activity

sun.store

Market outlook: firm demand supports a higher module price environment

March data suggest that demand remains stable, but is becoming more price-sensitive. Support is currently strongest in next-generation and premium module segments, where buyers appear willing to accept higher prices. At the same time, the inverter market remains balanced, with only minor monthly fluctuations and no signs of price pressure.

Solar offsets €3.76 billion in EU gas imports amid Middle East conflict

The key developments in March are:

- Increasing module prices in almost all major monitored categories

- Continued high prices for TOPCon modules

- Strong price growth for back-contact modules

- Overall stability in inverter prices, with a slight weakening in the hybrid segment and a slight strengthening in the grid-connected product segment

- Continued strong purchasing sentiment, with the PMI at 68

Taken together, these trends point to a market that is not overheating but is supported by sustained demand and a continued shift towards higher-value technologies. (hcn)