Despite the softer PMI reading, module prices continued to rise sharply across nearly all monitored segments. The strongest increases were once again concentrated in premium and higher-efficiency technologies, while the inverter market remained broadly stable, with only symbolic month-on-month changes.

Solar module market: premium and TOPCon segments continue to lead

April brought another strong month for module pricing, confirming that the upward trend seen in February and March has carried into Q2. The strongest increases were concentrated in modules below 500 Wp, suggesting that residential demand and premium-oriented installations remain the key drivers of current market activity.

TOPCon technologies continued their upward trajectory:

· TOPCon bifacial: €0.117/Wp (+9% m/m)

· TOPCon monofacial: €0.121/Wp (+6% m/m)

The data confirm that TOPCon remains the dominant technology across the European PV market. After several consecutive months of price growth, TOPCon modules are now trading significantly above late-2025 levels, reflecting both strong market acceptance and continued demand for higher-efficiency products.

March PV Index – prices rise with early signs of correction

Premium and design-focused categories also recorded another month of increases:

· Full Black modules: €0.124/Wp (+9% m/m)

· Back Contact modules: €0.129/Wp (+9% m/m)

Back Contact modules once again remained the highest-priced segment in the index, reinforcing the continued willingness among buyers to pay a premium for aesthetics, efficiency and high-performance residential solutions. Full Black modules followed a similar trend, showing that demand for premium residential products remains strong.

Brand rankings: leadership remains concentrated among Tier-1 suppliers

The competitive landscape among module manufacturers remained broadly stable in April, with Tier-1 suppliers continuing to dominate European distribution channels.

Based on power sold, the top five module brands in April were:

1. Trina Solar

2. JA Solar

3. LONGi

4. Jinko Solar

5. Canadian Solar

Trina Solar maintained its leading position for another consecutive month, confirming strong transactional momentum across European channels. JA Solar also remained among the top performers, while LONGi strengthened its position after weaker rankings earlier in the year. Jinko Solar stayed firmly within the leading group, while Canadian Solar continued to hold its place in the top five despite growing competition from rapidly expanding premium-focused manufacturers such as Aiko.

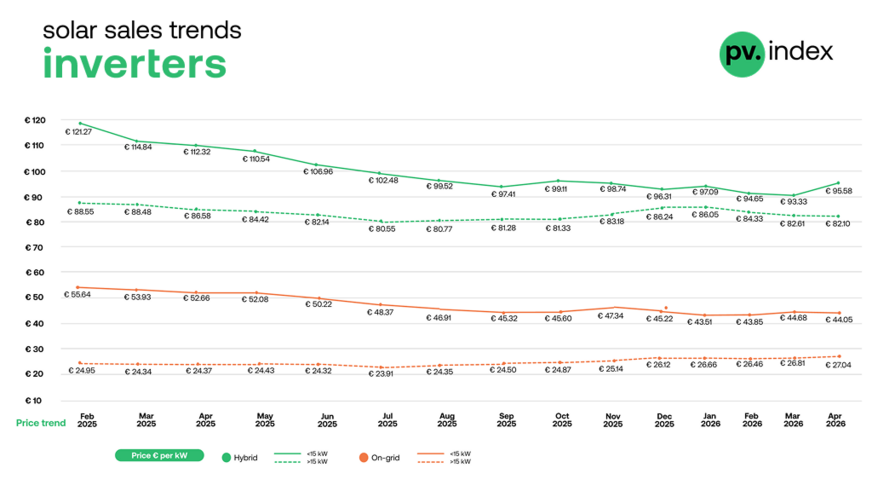

Inverters: pricing remains exceptionally stable

While module prices continued to rise, the inverter market remained remarkably stable in April. Month-on-month changes across all major segments were limited to around 1–2%, reinforcing the view that inverter pricing has entered a period of relative equilibrium.

sun.store

Hybrid inverters

· 1–15 kW: €95.58/kW (+2% m/m)

· >15 kW: €82.10/kW (–1% m/m)

Small hybrid systems recorded a modest increase in April, while larger systems continued to soften slightly. Overall, pricing dynamics in the hybrid segment remain very stable, supported by continued structural demand for storage-compatible systems.

String/on-grid inverters

· 1–15 kW: €44.05/kW (–1% m/m)

· >15 kW: €27.04/kW (+1% m/m)

The on-grid segment also remained broadly balanced. Smaller systems recorded a slight decline, while larger commercial systems moved marginally higher. Unlike the module market, there are currently no signs of significant variability or aggressive repricing among inverter manufacturers.

Inverter brand rankings: Sungrow moves into the leading position

Hybrid inverters

1. Deye

2. Huawei

3. GoodWe

4. Sungrow

5. Fronius

Deye maintained its clear leadership in the hybrid segment, supported by strong positioning in storage-ready installations and highly competitive pricing. Huawei continued to hold second place, while GoodWe strengthened its position within the top three. Sungrow and Fronius completed the leading group.

String/on-grid inverters

1. Sungrow

2. Huawei

3. Fronius

4. SMA

5. SolarEdge

April brought one of the first major leadership changes in the string inverter segment after a long period of Huawei dominance. Sungrow moved into the number one position, reflecting strong transactional activity and growing competitiveness across European distribution channels. Huawei slipped to second place, while Fronius strengthened its position within the top three.

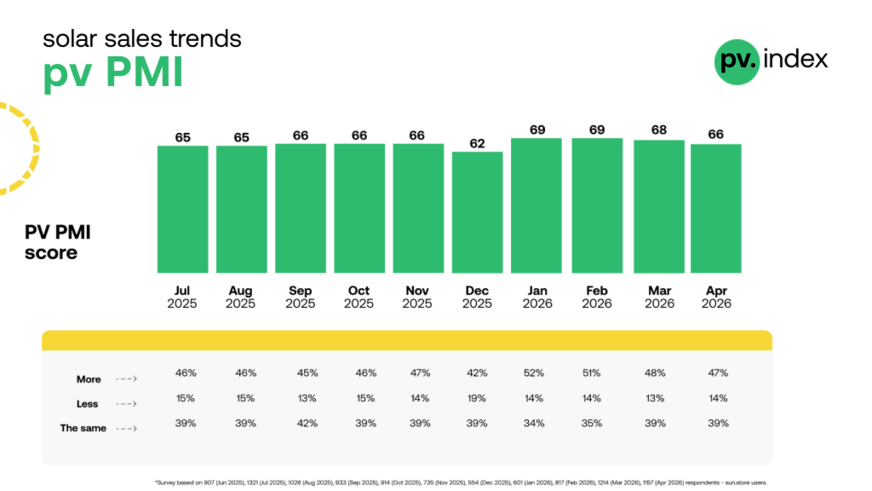

PV PMI: sentiment remains positive despite softer momentum

The PV Purchasing Managers' Index declined to 66 in April, marking the first more visible moderation after the exceptionally strong start to 2026.

sun.store

Survey results among 1,157 sun.store users show:

· 47% expect to increase purchases

· 39% expect no change

· 14% expect reduced purchasing activity

Market outlook: rising prices meet moderating demand

April data suggest that the European PV market is entering a more balanced phase. Module prices continue to rise, especially in premium and TOPCon segments, but demand momentum is beginning to cool after a very strong Q1.

Solar prices steady, new risks loom

The strongest pricing support remains concentrated in residential-oriented and premium module categories, particularly below 500 Wp. At the same time, inverter pricing remains exceptionally stable, suggesting a market currently less exposed to supply-side volatility.

The key developments visible in April include:

· continued module price increases across premium and TOPCon categories

· strong pricing momentum in residential-focused segments

· a further decline in the relevance of PERC technology

· broadly stable inverter pricing across all segments

· softer, but still expansionary, PMI sentiment

· growing competitive pressure among leading inverter manufacturers

(hcn)