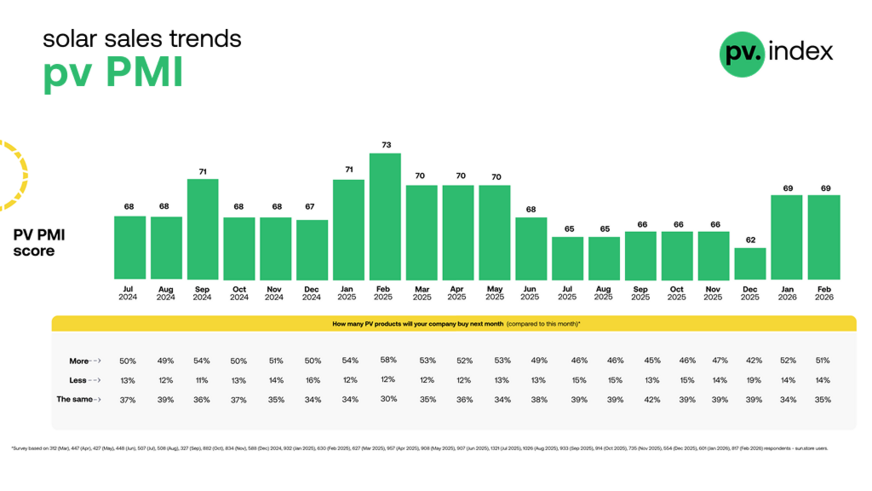

Demand for solar components remains robust across Europe. The PV Purchasing Managers’ Index (PMI) reached 69, its highest level since May 2025, indicating that installers and distributors are actively buying.

Price trends diverge across technologies. Newer module types such as TOPCon continue to gain pricing support, while older technologies like PERC remain broadly stable. In the inverter segment, prices moved only slightly, pointing to a balanced market.

Solar modules – next-generation technologies gain pricing strength

February pricing signals a gradual but visible shift in technology preferences across the European PV market. While legacy technologies remain broadly stable yet structurally under pressure, next-generation solutions are beginning to gain stronger pricing support. TOPCon bifacial prices are now nearly 20 percent above their mid-2025 trough, underlining the strengthening position of next-generation module architectures.

TOPCon technologies recorded clear price increases:

● TOPCon bifacial: €0.103/W (+9 percent month on month)

● TOPCon monofacial: €0.109/W (+10 percent month on month)

Design-focused and premium technologies also moved higher in February:

● Full Black modules: €0.108/W (+8 percent month on month)

● Back Contact modules: €0.107/W (+7 percent month on month)

These categories continue to demonstrate pricing resilience, supported by residential demand where aesthetics and performance remain important differentiators beyond simple cost.

- PERC: €0.077/W (unchanged)

While February transactions suggest slightly higher prices in isolated cases, the limited sample size means the benchmark index remains unchanged, reinforcing the view that PERC pricing has remained broadly stable since mid-2025.

KEY 2026 – Tailwind for the solar transition from Rimini

Brand rankings: leadership rotates again

February brought another reshuffle among the leading module brands, highlighting the dynamic competition among Tier-1 manufacturers.

1. JA Solar

2. Longi

3. Trina Solar

4. Jinko Solar

5. Canadian Solar

JA Solar moves into the leading position, reflecting strong transactional momentum and consistent availability across major European distribution channels. Longi holds second place, maintaining its reputation for stable supply and product reliability, while Trina Solar moves into third.

Jinko Solar, which frequently led the ranking over the past year, slips to fourth, pointing to short-term channel rotation rather than a fundamental loss of competitiveness. Canadian Solar rounds out the top five, reinforcing the market’s concentration among a small group of global manufacturers.

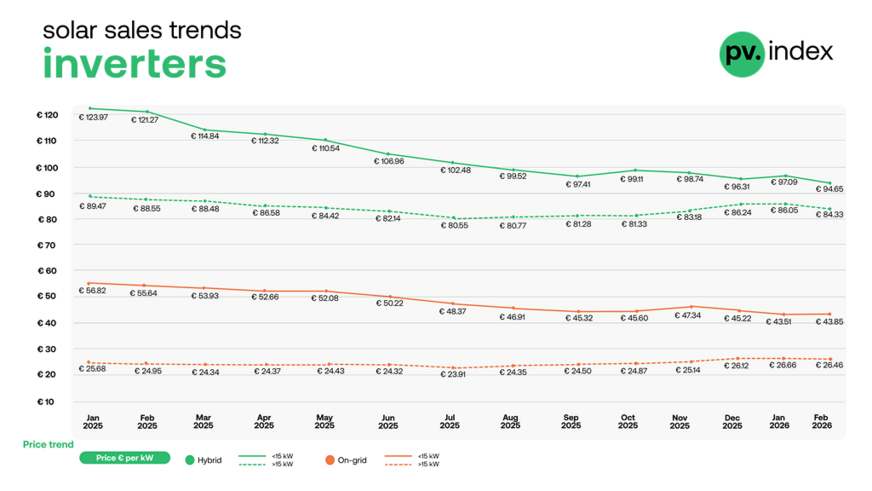

Inverter prices broadly stably

Hybrid inverters

● 1–15 kW: €94.65/kW (–3 percent month on month)

● >15 kW: €84.33/kW (–2 percent month on month)

Hybrid inverter prices softened slightly compared with January, although the correction remains modest. The segment continues to benefit from structural demand linked to energy storage adoption, helping prevent stronger price pressure.

String inverters

● 1–15 kW: €43.85/kW (+1 percent month on month)

● >15 kW: €26.46/kW (–1 percent month on month)

In the string inverter category, smaller residential systems showed a slight recovery, suggesting that the earlier price correction may be nearing its floor. Larger systems remained broadly stable, reflecting steady procurement activity in commercial and industrial projects.

sun.store

Overall, inverter prices remain broadly stable, with no signs of aggressive discounting despite ongoing competition among manufacturers.

Inverter brand rankings: leadership remains anchored

Hybrid inverters

1. Deye

2. Huawei

3. Fronius

4. GoodWe

5. Sungrow

Deye retains its leading position in the hybrid segment, benefiting from strong price-performance positioning and growing demand for hybrid-ready systems compatible with energy storage installations. Huawei holds a strong second place, while Fronius moves into third. GoodWe and Sungrow complete the top five, reflecting a competitive but relatively stable market structure.

String inverters

1. Huawei

2. Sungrow

3. SMA

4. Fronius

5. SolarEdge

Huawei continues its dominance in the string inverter category, maintaining the top position throughout the analysed period. Sungrow holds second place, followed by SMA. Fronius and SolarEdge remain firmly established among the leading brands in the segment.

PV PMI: sentiment remains firmly positive

The PV Purchasing Managers’ Index (PMI) reached 69 in February, confirming continued optimism among market participants.

Survey results among 817 sun.store users indicate:

● 51 percent expect to increase purchases

● 35 percent expect no change

● 14 percent expect reduced purchasing activity

This distribution places the PMI well above the neutral threshold of 50 and suggests that the European PV market continues to show solid transactional momentum despite technology-specific price adjustments.

sun.store

Market outlook – stability with technological transition

February data show a stable market where newer technologies are gradually gaining importance.

Key developments include:

● strengthening prices for next-generation module technologies such as TOPCon

● broadly stable PERC pricing, although the technology continues to lose relevance as the market shifts toward higher-efficiency architectures

● stable inverter prices with only modest segment corrections

● sustained dominance of global Tier-1 manufacturers

● strong buyer sentiment reflected in the PMI reading of 69

Rather than signalling volatility, these trends suggest a market gradually transitioning toward higher-efficiency technologies and more integrated PV systems.

Modules and batteries set for mild price uptick in 2026

Summary – key takeaways

- Modules: next-generation technologies gain price support, while PERC remains a declining legacy technology.

- Inverters: hybrid systems soften slightly, while string inverter prices stabilise.

- Brand rankings: leadership rotates among Tier-1 module suppliers; Huawei and Deye maintain inverter leadership.

- PMI: remains strong at 69, confirming sustained purchasing momentum across the European PV market. (hcn)