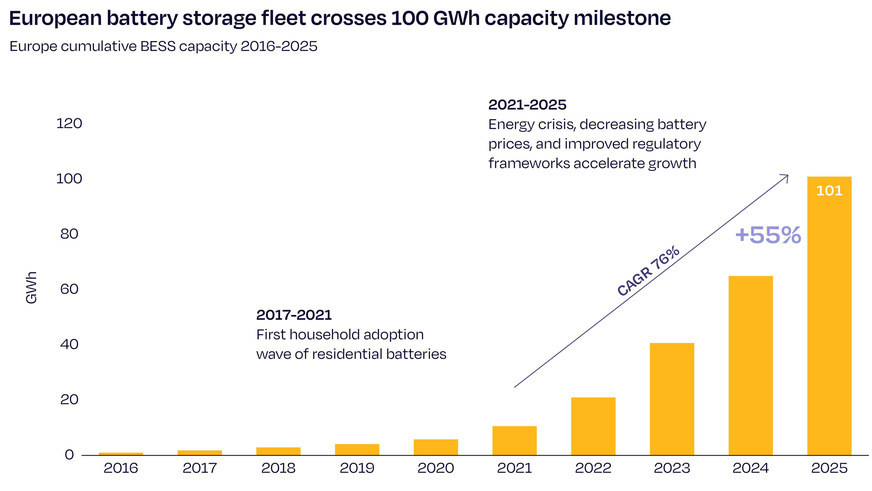

Europe installed 36 GWh of new battery storage capacity in 2025, pushing total operational capacity beyond 100 GWh for the first time and extending a run of consecutive annual growth to twelve years. The annual growth rate came in at 48%, a rebound from a slower 2024, according to SolarPower Europe's European Battery Market Outlook 2026–2030. Within the EU-27, 27 GWh was installed across the bloc – 75% of total European additions – bringing cumulative EU capacity to almost 80 GWh by year-end.

SolarPower Europe

Utility-scale crosses the halfway mark

The defining shift in 2025 was the emergence of utility-scale storage as the market's largest annual segment. Large-scale systems accounted for more than half of new installations for the first time, driven by growing grid flexibility requirements, stronger revenue stacking opportunities, falling technology costs, the expansion of hybrid solar-plus-storage projects and rising investor confidence. The 2024 slowdown had already signalled the direction of travel: utility-scale growth that year offset a contraction in residential demand, itself a correction following the exceptional expansion triggered by the 2022 energy crisis.

After the spike – why solar and battery prices will cool again

Market geography: the top five shifts

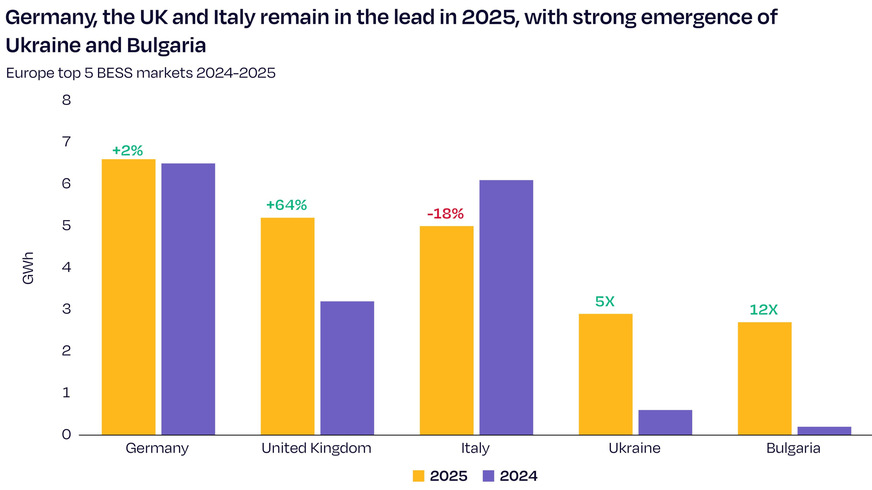

Germany, the UK and Italy retained the top three positions in 2025, though their collective share of European installations fell from around 80% in 2024 to 62%, as deployment broadened across smaller markets. Ukraine and Bulgaria entered the top five, each adding almost 3 GWh. Germany grew by just two percent; Italy contracted by 18% as investors held back ahead of the first round of the country's MACSE auction scheme; the UK rebounded after a 14% decline in 2024 caused by reduced grid-scale revenues. Ukraine's rapid rise reflects the strategic role battery storage has taken on following extensive damage to the country's power infrastructure.

SolarPower Europe

Cumulative fleet: composition shifting

Europe's total installed battery fleet reached just over 100 GWh by the end of 2025, a tenfold increase since 2021. Residential storage still accounts for just under half of cumulative capacity but has lost share for two consecutive years. Utility-scale has risen to become the second-largest segment and is on course to overtake residential in 2026. Commercial and industrial storage remains stable at around 11% of the total fleet. The EU's solar-to-battery ratio improved from 10:1 in 2024 to 8:1 in 2025, though SolarPower Europe flags this as still insufficient relative to the scale of solar generation on the system.

Michael Villa: "Demand side flexibility is a strategic asset"

Outlook to 2030: fourfold growth projected, but a gap remains

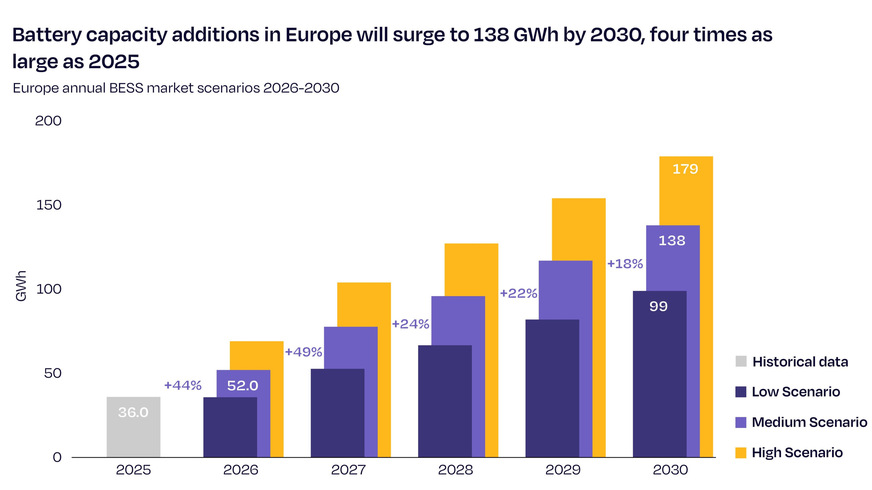

Under SolarPower Europe's medium scenario, annual installations are projected to exceed 50 GWh in 2026 – a 44% increase on 2025 – rising to 138 GWh by 2030, a compound annual growth rate of 28% over the period. Utility-scale will account for close to two-thirds of annual additions by 2026 and around 67% of total installed capacity by 2030. Residential demand is expected to recover gradually, supported by the wider availability of dynamic tariffs and growing consumer interest in self-sufficiency, reaching 13.2 GWh in 2026. The C&I segment is forecast to add nearly 6 GWh in 2026, growing at 26% annually.

SolarPower Europe

By 2030, Europe's cumulative fleet is projected to reach 582 GWh under the medium scenario, with the EU-27 accounting for 470 GWh. Both figures fall short of the 600 GWh modelled by Rystad Energy as the level required to meet EU climate, energy security and affordability targets. Only the high scenario, at 593 GWh, approaches that threshold. The EU's own 200 GW storage target for 2030, set under the AccelerateEU framework, is also unlikely to be met under the medium scenario.

Intersolar – Solar's success is a new headache for European grids

Policy gap

SolarPower Europe is calling for a dedicated EU Battery Storage Action Plan to close what it describes as a structural flexibility gap. The three priorities it identifies: reforming network tariff structures to properly reward flexibility; ensuring non-discriminatory market access for battery storage; and providing long-term policy consistency to support investor confidence. (TF)